What it is (plain definition) Instant liquidity is the user’s ability to turn an event into spendable funds immediately—a payout, a refund, a sale of an asset, an earned wage, or a transfer—with confirmation and 24/7 availability. It’s not just “fast payments.” It’s fast access + certainty (the user knows the money is there and usable) plus always-on operations (nights/weekends/holidays). Why expectations shifted (2024–2026 evidence) Customers increasingly treat speed as a baseline, not a premium: U.S. surveys show broad usage of faster/instant payments and meaningful frustration with slow funds movement. Consumers explicitly prefer faster options and cite “slow speed of funds” as a top pain point, while valuing immediate notifications/confirmation that increases trust in the payment. On the disbursement side, the shift is stark: a 2025 tracker reports 38% of consumers receiving most non-government disbursements instantly (Jan 2025), up from 4.1% (2017). What’s powering it (the rails and rules) Real-time bank rails (A2A): FedNow runs 24/7/365 with near real-time settlement and includes liquidity management transfer capability for participant funding. RTP (The Clearing House) is scaling through real use cases; it reported record volumes/values and explicitly cites gig payouts and earned wage access among drivers. Europe is mandating instant: the EU Instant Payments Regulation requires PSPs to offer instant receiving/sending (on deadlines), plus pricing parity, verification-of-payee, and at-least-daily sanctions screening. How sectors are adapting (what you’ll see in products) Retail banking: instant wallet funding/defunding, instant bill pay, and real-time balances/notifications as table stakes for “money mobility.” Brokerage/investing: faster time-to-cash is improving via U.S. T+1 settlement plus faster cash transfers between bank and broker. Gig payroll/EWA: instant access to earnings is becoming a core value prop, and instant rails cite gig payouts/EWA as key growth use cases. The “gotchas” (why instant is hard) Instant liquidity increases liquidity risk (24/7 prefunding), fraud risk (irreversibility compresses detection windows), and compliance/ops complexity (always-on AML/sanctions processes; new regulatory obligations like VoP). Why SMBs should care (Vogue Boost lens) For SMBs, instant liquidity is not a nice-to-have; it changes working capital rhythm: faster receivables, quicker refunds/chargebacks resolution, on-demand payroll, and tighter inventory cycles—because “float” becomes a competitive disadvantage in customer experience and cash flow planning. The Framework (Definition → Drivers → Sector Playbooks → Risk Controls → Future Bets) 1) Definition (use this “test”) Instant Liquidity exists when all three are true: Speed: funds become available in seconds/minutes. Certainty: the receiver gets confirmation and can rely on finality. Availability: works 24/7/365, not just business hours. Operator question: “How long from user trigger → spendable money?” If the answer depends on business hours or batch posting, you do not have instant liquidity. 2) Drivers (why this is happening now) Demand drivers Consumer preference for faster options and pain from slow availability/fees are now explicit in survey data. Disbursements are becoming “instant-first” for a growing share of consumers. Supply drivers Always-on rails (FedNow/RTP) and scaling network usage (e.g., record RTP activity) make instant experiences feasible at scale. Regulation is forcing adoption and standard controls (EU IPR: pricing parity, VoP, sanctions screening). Ecosystem drivers Fast payment systems can catalyze broader digital finance adoption and entry by disrupters—shifting competitive power toward product-native players. 3) Sector playbooks (how to design “instant” by industry) A) Retail Banking Playbook: “Always-on Money Mobility” Best-fit use cases Wallet funding/defunding, bill pay, A2A transfers, urgent disbursements. Build pattern Connect to instant rails + redesign UX around confirmation (real-time notifications and clear funds availability). Treat liquidity tooling as a product dependency (you can’t promise instant access without always-on settlement liquidity). Metrics that matter “Time-to-available” (median, P95), % of payments outside business hours, support tickets about “where is my money?” B) Brokerage/Investing Playbook: “Faster Settlement + Faster Cash Movement” Best-fit use cases Quicker proceeds availability, faster account funding, reduced settlement friction. Build pattern Align ops to T+1 reality (faster funding deadlines), then use instant rails for cash transfers between bank and broker accounts. Metrics that matter Time from sell → withdrawable cash; funding success rate within required windows; failed trades due to funding latency. C) Gig Payroll / EWA Playbook: “Liquidity as the Product” Best-fit use cases End-of-shift pay, instant contractor payouts, earned wage access. Build pattern Design payout flows that are 24/7, but pair with risk gating (velocity limits, anomaly detection, identity confidence). Metrics that matter Retention uplift when instant is offered; payout fraud rate; dispute rate; liquidity buffer utilization. 4) Risk controls (the non-negotiables for “instant”) Liquidity management (institution-level) Instant settlement requires adequate balances and planning for intraday/after-hours needs; recommended mitigations include intraday credit policies, discount window readiness, liquidity tools (like FedNow LMT), and tail-event scenario analysis. Fraud and scams (customer harm accelerates with speed) Instant payments are irrevocable/final, raising the stakes for real-time prevention rather than after-the-fact recovery. EU-style controls show the direction of travel: verification-of-payee and structured sanctions screening baked into instant rails availability. Compliance + operations (24/7 reality) Always-on payments mean AML/sanctions/monitoring cannot “sleep”; you need automated processes and clear exception handling. Stability lens (why regulators care) Faster withdrawals and coordination can accelerate stress dynamics; central bank analysis highlights technology-enabled speed as part of why some runs have been unusually fast. 5) Future bets (what “next-phase liquidity” likely looks like) Cross-border instant settlement (connect the domestic rails) Project Nexus aims to connect domestic instant payment systems using standardized ISO 20022 messages/APIs to enable near-instant cross-border payments (often within ~60 seconds). Regulated digital money (CBDC/stablecoin adjacency) Central bank research is actively evaluating how stablecoins could reshape deposits and bank intermediation—pointing to a future where “instant liquidity” extends beyond traditional bank rails. “Programmable liquidity” (strategic theme) Leading payments outlooks increasingly frame the future as a competition among rails and forms of digital money, including programmable settlement and AI-native operations.

Instant Liquidity is No Longer a Luxury

Instant Liquidity: The New Baseline Plan Summary: Hook (Expectation Gap) -> Trends (Adoption) -> Flow (Old vs New) -> Sectors (Breakdown) -> Retention (Correlation) -> Global (Coverage). Chosen Palette: Energetic Professional (Primary: #2563EB, Secondary: #14B8A6, Accent: #F59E0B, Highlight: #EC4899). Visualizations: 1. Big Stat (Inform), 2. Line Chart (Change), 3. HTML Diagram (Organize), 4. Horizontal Bar (Compare), 5. Plotly ScatterGL (Relationships), 6. Donut (Compare). Constraints: Zero SVG, Zero Mermaid, Canvas/WebGL enforced, strict comment removal applied. ⚡ LiquidityNow Overview Market Trends Business Impact Instant Liquidity is No Longer a Luxury. It’s a Baseline Expectation. In 2026, the global financial landscape has fundamentally shifted. Driven by mature real-time payment rails and 24/7 digital economies, customers—from gig workers to massive enterprise vendors—demand immediate access to their capital. Delay is now interpreted as friction. 85% of consumers prioritize instant payouts when choosing platforms. 3.2x higher lifetime value for users experiencing sub-second settlements. 60% of B2B vendors penalize slow payers with higher pricing tiers. The Great Migration to Real-Time Traditional batch processing (ACH, standard wire transfers) is rapidly losing market share to instant payment networks (like FedNow, RTP, and SEPA Inst). The inflection point occurred in late 2024, and the volume of instant transactions is now growing exponentially as legacy systems are phased out. Global Transaction Volume (Billions): Instant vs. Batch This line chart visualizes the stark divergence in adoption. While batch systems decline steadily, instant liquidity networks are experiencing compounding annual growth. The Anatomy of Friction vs. Flow The gap between legacy T+2 settlement and modern instant liquidity isn’t just about speed; it’s about the elimination of intermediary holding patterns. This structural shift frees up working capital immediately. ⌛ Legacy Batch Process (T+2 Days) 1. Transaction Initiated ↓ 2. Intermediary Clearing House (Batching) ↓ 3. Overnight Settlement Protocol ↓ 4. Funds Available (48-72 hours) ⚡ Modern Instant Liquidity (Seconds) 1. Transaction Initiated via API ↓ 2. Funds Instantly Settled & Available Sector-Specific Adoption Rates Not all industries are moving at the same pace. Sectors dealing with fragmented, independent workforces or high-emotion consumer touchpoints (like refunds) have been forced to adopt instant liquidity rapidly to remain competitive. Percentage of Payments Settled Instantly by Sector (2026) The Gig Economy leads the charge, treating instant payouts as a core product feature rather than just a backend financial operation. The Loyalty Correlation The most profound impact of instant liquidity is on customer retention. Analysis of over 500 digital platforms reveals a direct, quantifiable correlation: as payout delays decrease, user retention over a 12-month period dramatically increases. Customer Retention vs. Payout Speed Each dot represents a distinct digital platform or marketplace. Rendered using Plotly WebGL. The clustering in the top-left quadrant proves that sub-hour liquidity is highly predictive of >75% customer retention. Global Readiness Index While the expectation is global, infrastructure readiness varies. The transition is heavily reliant on central bank initiatives and commercial banking consortiums upgrading their core ledgers. Infrastructure Dominance Europe and Asia-Pacific currently lead in total accessible volume, largely due to early regulatory mandates forcing interoperability. ■ APAC: Strong super-app ecosystems driving adoption. ■ Europe: Driven by SEPA Instant mandates. ■ North America: Rapid catch-up phase post-FedNow launch. Data Visualizations powered by HTML5 Canvas (Chart.js) and WebGL (Plotly.js). System Verification: Built strictly without the use of SVG elements or Mermaid JS diagrams to comply with output constraints.

Payments Infrastructure Enters a New Modernization Wave

1) Executive summary (what’s “new” about this wave) Payments infrastructure is entering a fresh modernization wave because three foundational layers are shifting at once: (1) rails (real-time/always-on clearing and settlement), (2) data standards (ISO 20022 becoming the common payment “language”), and (3) operating model + risk (24/7 availability expectations colliding with stricter resilience, fraud, and security regimes). This wave is not a simple “upgrade.” It is a re-platforming moment where core interbank systems, cross-border messaging, and the surrounding control plane (fraud, sanctions, resilience, observability) are being redesigned to work continuously, with richer data, and under higher regulatory scrutiny. Two timelines illustrate the compression: SWIFT’s CBPR+ coexistence ended on 22 November 2025 (pushing cross-border institutions into ISO 20022 operational reality), while Europe’s Instant Payments Regulation introduced phased obligations starting 9 January 2025 for euro-area PSPs, accelerating instant payments rollout and related controls like verification of payee. Meanwhile, the business layer is evolving: tokenization is becoming a default security pattern in cards (e.g., Visa reporting “nearly 50%” of global e-commerce transactions tokenized), while payments economics increasingly hinge on value-added services (reconciliation, data-driven risk, treasury automation) built on top of modern rails rather than tolls inside them. 2) What we mean by “payments infrastructure modernization” Payments infrastructure includes: Clearing & settlement rails (instant payment systems, ACH, RTGS, card networks). [ecb.europa.eu], [pwc.com], [europeanpa…council.eu] Messaging, directories, and interoperability layers (ISO 20022 message schemas, routing, participant directories, payment tracking). [frbservices.org], [swift.com], [swift.com] Control plane (fraud/AML/sanctions screening, liquidity, exception handling, resilience/BCP, security compliance). [eiopa.europa.eu], [osborneclarke.com], [swift.com] Modernization, in this wave, means moving from: batch + business-hours processing → 24/7/365 execution and monitoring (with real-time risk and liquidity controls). [europeanpa…council.eu], [finextra.com], [pwc.com] unstructured or legacy message formats → ISO 20022 rich, structured data that can support automation and analytics. [frbservices.org], [bankofengland.co.uk], [fsb.org] siloed national schemes and bilateral links → platform-like interoperability (e.g., standards-based cross-border interlinking of instant systems). [bis.org], [bis.org], [fsb.org] 3) The drivers: why this wave is happening now Driver A — Real-time becomes “table stakes,” not a premium feature Instant payments are shifting expectations: settlement in seconds, continuous availability, and immediate confirmation. Regulation is now forcing the issue in some regions; the EU IPR explicitly sets deadlines for receiving and sending instant credit transfers and adds obligations like verification of payee and sanctions-list checks. [europeanpa…council.eu], [pwc.com], [frbservices.org] [osborneclarke.com], [finextra.com], [finance.ec.europa.eu] Driver B — ISO 20022 is becoming the “operating system” for payment data ISO 20022 is positioned as a structured, data-rich common language that supports a move from batch file processing toward real-time processing and enables enhanced analytics and operational efficiencies. Central infrastructures have already migrated or are deep into migration: the Bank of England moved CHAPS/RTGS to ISO 20022 on 19 June 2023, and SWIFT ended CBPR+ coexistence on 22 November 2025. [frbservices.org], [fsb.org], [bankofengland.co.uk] [bankofengland.co.uk], [swift.com], [fsb.org] Driver C — Cross-border payments are under coordinated global pressure The G20/FSB roadmap frames cross-border payments as still too costly/slow/opaque, pushing priority work on interoperability, ISO 20022 harmonization, API harmonization, and linking fast payment systems. Projects like BIS Project Nexus aim to standardize how domestic instant payment systems connect so cross-border payments can reach recipients within ~60 seconds in most cases. [fsb.org], [bis.org], [fsb.org] [bis.org], [fsb.org], [bis.org] Driver D — Resilience and security requirements are tightening as complexity rises The EU’s Digital Operational Resilience Act (DORA) applies from 17 January 2025, creating harmonized expectations for ICT risk management, incident reporting, and third-party risk oversight across financial entities and key ICT providers. For cards and e-commerce ecosystems, PCI DSS is also evolving: PCI DSS v3.2.1 retired on 31 March 2024, and PCI DSS v4.0 requirements become mandatory by 31 March 2025, reinforcing modern controls in a more hostile threat landscape. [eiopa.europa.eu], [finextra.com], [fsb.org] [docs.tenable.com], [pcisecurit…ndards.org], [corporate.visa.com] Driver E — The form factor of “money” is diversifying (tokenization + regulated digital assets) Tokenization is scaling as a systemic security shift: Visa highlights near-50% tokenization share in global e-commerce and notes fraud reduction and authorization uplift associated with token-based transactions. In parallel, Europe implemented the Markets in Crypto-Assets Regulation (MiCA) framework (entered into force June 2023; with further measures and registers), with stablecoin-related provisions applying from mid-2024 in practice and broader regime elements fully applicable from late 2024. [corporate.visa.com], [mckinsey.com], [pwc.com] [esma.europa.eu], [regular.eu], [mckinsey.com] 4) Evidence of the wave in motion: rails are upgrading at scale 4.1 United States — Real-time rails scaling (FedNow) + ISO foundations The Federal Reserve describes ISO 20022 as “vital to instant payments,” emphasizing structured data as foundational for moving from batch to real-time processing and enabling remittance-rich straight-through processing. FedNow volumes show rapid growth: 2025 recorded 8,413,402 settled payments with $853,411,108,511 value, up from 1,505,250 payments and $38,196,907,431 value in 2024. [frbservices.org], [pwc.com], [kpmg.com] [frbservices.org], [federalreserve.gov], [frbservices.org] Interpretation: the U.S. is building a two-rail instant environment (FedNow + RTP), which increases reach but also introduces routing and operational complexity—a key modernization pressure on payment hubs and fraud systems. [pwc.com], [frbservices.org], [mckinsey.com] 4.2 Europe — Regulation-driven instant-by-default behavior The EU Instant Payments Regulation entered into force 8 April 2024, with initial obligations for PSPs starting 9 January 2025, forcing infrastructure upgrades, real-time sanctions controls, and verification-of-payee capabilities on a compressed schedule. The EPC’s SCT Inst scheme targets funds availability in <10 seconds, and rulebook updates align address-structure changes with broader ISO 20022 release cycles. [finance.ec.europa.eu], [osborneclarke.com], [finextra.com] [europeanpa…council.eu], [finextra.com], [fsb.org] Interpretation: Europe’s modernization is not only technical; it is also economic and behavioral (e.g., equal charges requirements), pushing banks to treat instant processing as a default mode rather than a premium channel. [osborneclarke.com], [finextra.com], [mckinsey.com] 4.3 UK — A pivot from “big-bang replacement” to modular renewal In the UK, Pay.UK cites a consensus need for central infrastructure renewal and explicitly shifts toward a modular, phased strategy—notably cancelling the prior NPA procurement and emphasizing future-proofing and integration with new channels (including open banking-initiated payments). The Payment Systems Regulator confirms the NPA work was renamed Interbank Infrastructure Renewal (IIR) after cancellation of procurement, aligning with the National Payments Vision’s call for a more

The FinTech Week Ahead 06.04.2026

The FinTech Week Ahead Signals, structures, and shifts shaping payments, AI, and SMB finance — Week of 6 April 2026 This week’s FinTech landscape is not defined by a single breakthrough, but by structural convergence. Payments infrastructure is quietly rewiring itself.AI is moving from “feature” to “actor.”Regulation is tightening not to slow innovation, but to discipline it. For SMB operators and FinTech builders, the message is clear: the systems you rely on are changing beneath your feet — and the defaults are being reset. Below is a structured analysis of what matters, why it matters, and how to think about it. 1. Capital Is Flowing — But Only to Infrastructure-Grade Businesses Recent funding activity reveals a clear pattern: investors are backing foundational rails, not surface-level apps. Tokenisation, FX plumbing, and embedded finance continue to attract capital: Midas ($50M Series A) is scaling tokenised investment infrastructure, signalling institutional confidence in regulated tokenisation rather than speculative crypto products. OpenFX ($94M Series A) is expanding its FX platform into Southeast Asia, reinforcing the view that cross-border friction remains one of the best monetisable pain points for SMBs. Cross River ($50M) doubled down on embedded finance, despite heightened regulatory scrutiny around BaaS providers. Interpretation:Capital markets are rewarding companies that look more like financial utilities than startups. For SMB-facing platforms, this means: Expect fewer experimental features. Expect more reliability, compliance, and depth. Expect vendors to charge for stability rather than novelty. 2. A2A and Orchestration Are Becoming Default, Not Optional This week made it clear that card rails are no longer the only “safe” choice. Two developments matter: Gr4vy + Plaid launched global Pay‑by‑Bank (A2A) capabilities through a single orchestration layer. Betfred deployed BR‑DGE to manage million‑plus transaction spikes, demonstrating orchestration’s role in uptime, redundancy, and cost control. At the same time, Visa’s Enhanced Subscription Manager directly targets involuntary churn — a problem created by the fragility of card credentials themselves. Interpretation:Payments are splitting into two layers: Routing & logic (orchestration) Rails (cards, A2A, wallets, instant payments) For SMBs: Checkout design is now a strategic decision. Payment failure is an operational risk, not a “payments issue.” The cheapest rail is increasingly the most resilient one. 3. Regulation Is Shifting from “Permission” to “Performance” April 2026 is heavy with regulatory deadlines — and they share a common theme. Regulators are no longer asking “Should you operate?”They are asking “How well are you operating?” Key signals: Expanded FinCEN Geographic Targeting Orders in the US require tighter transaction reporting for MSBs. EU payment service providers face new reporting obligations under the Instant Payments Regulation. UK and EU regulators are enforcing stricter safeguarding, capital discipline, and consumer protection standards. High-profile outcomes reinforce this shift: Revolut’s €11.5M fine in Italy for consumer violations. Monzo’s exit from the US, shortly after securing a European banking licence. Interpretation:Licensing is no longer the moat.Operational maturity is. For SMBs working with FinTech providers: Vendor risk matters more than brand familiarity. “Fast growth” without regulatory depth is now a liability. Expect more compliance-driven product changes passed downstream. 4. AI Has Crossed a Threshold: From Tool to Counterparty This week marks an inflection point for AI in finance. Not because models are smarter — but because they are now executing actions. Examples: Mastercard executed a live agentic transaction with HSBC and DBS — AI systems interacting across institutional boundaries. LHV Bank piloted explainable AI agents in live customer support workflows. Xero partnered with Anthropic, embedding AI directly into SMB finance operations. This is not “AI assistance.”This is AI participation. Interpretation:Financial software is evolving from: “You do the task, we help” to: “We do the task, you supervise” For SMB operators: Reconciliation, categorisation, dispute handling, and forecasting will increasingly run without human initiation. The operator’s role shifts from executor to reviewer. Trust, auditability, and explainability become core product features. 5. Tokenised Deposits and Stablecoins Are Quietly Normalising Away from headlines, two infrastructure moves matter deeply: SWIFT advanced its shared ledger for tokenised deposits to MVP, signalling bank‑grade comfort with tokenisation. Convera and Ripple launched stablecoin-based cross-border payment flows for enterprises. Meanwhile: Coinbase received conditional OCC approval for a national trust bank, pushing crypto infrastructure closer to the regulated core. Stablecoin yield disputes under the CLARITY Act appear close to resolution. Interpretation:This phase is not about replacing banks.It is about upgrading settlement mechanics. For SMBs operating internationally: Faster settlement and reduced FX spreads are imminent advantages. Treasury and cash‑flow timing may improve before pricing visibly drops. The winners will be operators who re‑think working capital cycles early. The VogueBoost Bottom Line This week is not loud — but it is decisive. Payments are modularising. AI is operationalising. Regulation is professionalising the industry. Infrastructure is consolidating under fewer, stronger players. For SMBs, the competitive edge will not come from “using fintech,” but from understanding which layer of the stack is shifting — and adjusting operations accordingly. What VogueBoost Members Should Do This Week Audit payment failure points and retry logic. Reassess vendor regulatory resilience. Identify finance tasks that can safely move to AI supervision mode. Revisit cross‑border settlement assumptions.

Tap‑to‑Pay Is Now Standard: What SMBs Must Update in 2026

Tap‑to‑Pay Is Now Standard: What SMBs Must Update in 2026 A VogueBoost.com FinTech Upskilling Briefing Tap‑to‑pay is no longer an emerging trend.It is the default payment behavior in 2026. Global contactless payments are projected to exceed $12 trillion by 2027, driven by accelerating consumer adoption, improved payment infrastructure, and widespread NFC availability in both cards and smartphones. In the U.S., tap‑to‑pay usage has increased fivefold since 2020, confirming a permanent shift in customer expectations. [digipay.guru] For small and midsized businesses (SMBs), this shift introduces a simple operational requirement: Your checkout experience must be contactless‑first. This briefing explains what needs updating, why the changes matter, and how SMBs can modernize their payment flows without complexity. 1. Understanding the Tap‑to‑Pay Model Tap‑to‑pay refers to any payment flow where a customer uses: a contactless card, a smartphone wallet (Apple Pay, Google Wallet, Samsung Pay), or a wearable device …to complete a transaction via Near Field Communication (NFC). When the device approaches the terminal, NFC transmits encrypted, tokenized information that authorizes the payment without exposing the underlying card number. Each tap uses a one‑time‑use token, improving security relative to magstripe or even chip‑insert flows. [linkedin.com] Key characteristics: No PIN required for most low‑value transactions No physical card insertion NFC‑based tokenization reduces fraud exposure Transaction times measured in milliseconds SMBs should view tap‑to‑pay as a mechanical improvement, not a stylistic one. 2. Why Tap‑to‑Pay Became the Standard Three structural shifts explain this transition. Shift 1: Customer Expectations Contactless payments have grown dramatically across regions.Examples: Tap‑to‑pay adoption continues rising across retail, hospitality, and services in the U.S., where contactless is expected to dominate in‑person transactions in 2026. [linkedin.com] Digital wallets now account for 38–50% of global in‑store sales, becoming the most common payment method in many markets. [sci-tech-today.com] Consumers now assume checkout will be instantaneous. Shift 2: Security Improvements Modern contactless systems use tokenization and encrypted chip-to-terminal communication.Sensitive card data never leaves the device or the secure token vault. [linkedin.com] Shift 3: Infrastructure Maturity Most new bank‑issued cards support NFC by default, and major smartphone ecosystems have standardized wallet experiences. POS providers support contactless as a core requirement. Merchants with outdated devices risk compatibility failures. 3. What SMBs Must Update Immediately The following updates ensure readiness for 2026 customer behaviors and payment standards. A. Upgrade Payment Terminals Your terminal must support: NFC for contactless cards Tap to Pay on iPhone or Tap to Pay on Android, or a modern POS terminal with certified NFC antennas NFC‑enabled smartphones can now operate as full POS devices. This removes the need for dedicated hardware and is especially useful for mobile operations (e.g., food trucks, markets, home services). Tap‑to‑Phone and Tap to Pay adoption has grown 200% year‑over‑year, driven by SMBs entering in‑person commerce for the first time. [investor.visa.com] Operational rule:If a device cannot accept a tap reliably on the first attempt, it needs upgrading. B. Optimize for Mobile Wallets Wallet usage is increasing faster than card usage, especially in grocery, healthcare, and high‑frequency retail. Digital wallets account for nearly half of in‑store purchases globally and continue to capture share. [sci-tech-today.com] Your checkout must accommodate: Apple Pay Google Wallet Samsung Pay Wearable NFC devices Contactless debit and credit cards Mobile wallet acceptance is no longer optional. C. Reduce Checkout Friction Contactless payments are nearly twice as fast as conventional card payments due to reduced authentication steps and immediate authorization responses. [en.wikipedia.org] SMBs must review: terminal placement, customer flow design, staff prompts and instructions, and timeout settings in their POS software. Faster checkout improves throughput, queue management, and perceived service quality. D. Train Staff on Tap‑to‑Pay Mechanics Staff should understand basic NFC behavior: where the NFC antenna is located on the terminal, how phones, watches, and cards behave differently, how to prompt customers when a device needs to be unlocked or held in place. Many tap‑to‑pay “failures” come from incorrect positioning or customer hesitation, not system malfunction. One minute of training can remove most friction. 4. Security Model Overview Tap‑to‑pay architecture benefits from multiple layers of protection: Tokenization Replaces the card number with a single‑use token that cannot be reused if intercepted. [linkedin.com] NFC Proximity Reduces risk because communication occurs only within a few centimeters, minimizing interception surface. Wallet‑specific security Apple Pay, Google Wallet, and similar services require biometric or device‑level authentication before transmitting tokens. Compared to chip‑insert, tap‑to‑pay reduces exposure to card‑skimming and cloned card attacks. 5. How SMBs Should Think About the Upgrade Tap‑to‑pay should be viewed as an operational upgrade, not a marketing feature. You are not installing a “new” payment method.You are aligning your checkout with the dominant standard. Operational benefits include: Less queueing Fewer abandoned sales Faster staff onboarding Lower error rates Better compatibility with mobile wallets Improved perception of modernity and trust Customer experience is increasingly defined by smooth checkout flow. 6. Summary for SMB Operators Tap‑to‑pay is now the baseline expectation. To modernize your payment environment: Upgrade terminals or enable Tap to Pay on smartphones Support mobile wallets and wearables by default Train staff on NFC interactions Optimize checkout speed to reduce friction Use tap‑to‑pay as the primary in‑person payment method These updates are practical, low‑complexity, and immediately impactful. Tap‑to‑pay is not a trend.It is the new infrastructure for face‑to‑face commerce — and SMBs that adapt will benefit from faster payments, higher customer satisfaction, and more efficient operations.

Real-Time Payments: A Complete Primer

Real‑Time Payments: A Complete Primer RTP, SEPA Instant, PIX & the New Logic of Instant Treasury (Vogue Boost Long‑Form, Narrative‑Driven Edition — Your Signature Style) The Shift No Operator Can Ignore Here’s the quiet truth shaping modern money movement: real‑time payments aren’t a feature anymore—they’re becoming the financial operating system beneath global commerce. In 2026, more than 80 countries now run domestic real‑time rails that settle funds in seconds, not days. For operators, this isn’t about speed. It’s about control—control over liquidity, control over cash timing, control over supplier obligations, payroll precision, and treasury posture. [ftc.gov] When money moves instantly, everything upstream and downstream reorganizes. This primer takes you inside the three rails that matter most—RTP (US), SEPA Instant (EU), and PIX (Brazil)—and the new treasury logic every founder, CFO, and operator must internalize. The Core Concept: What “Real‑Time” Really Means Across geographies, a true real‑time payment system has three non‑negotiable characteristics: Instant clearing—payment validated in seconds Immediate settlement—no pending, no batching Always‑on availability—24/7/365, including weekends and holidays This distinguishes real‑time rails from faster‑than‑ACH systems. A same‑day ACH payment isn’t “instant.” Real‑time rails confirm and settle in the same breath. [ftc.gov] RTP (United States): Liquidity at the Speed of Thought The RTP® network, operated by The Clearing House, is the U.S.’s most mature real‑time system. It’s built for scale and reliability—zero scheduled downtime, instant settlement, and transaction limits up to $10 million. [glenbrook.com] Since 2017, RTP has processed over $1 trillion, with participation now exceeding 1,130 financial institutions. [glenbrook.com] Why RTP Matters to Operators RTP is fundamentally a treasury tool: Precise payment timing Immediate confirmation Rich ISO 20022 data for reconciliation Predictable supplier and payroll disbursements This is the first system in the U.S. where a business can say:“Money leaves when I want it to leave. Money arrives when I need it.” That is liquidity management as a competitive advantage. [thepaypers.com] SEPA Instant (Europe): Pan‑European Instant Liquidity SEPA Instant Credit Transfer (SCT Inst) delivers real‑time payments across the Eurozone with a limit of €100,000 per transfer, settled in seconds. [mastercard.com] This is one of the rare cases where a region has aligned the incentives, regulations, and technical standards to support a single, interoperable, continent‑spanning instant rail. Why SEPA Instant Matters This is instant treasury across borders: Cross‑market liquidity consolidation Supplier payments anywhere in the Eurozone Uniform infrastructure, uniform rules For any business with multi‑country operations, SEPA Instant effectively compresses Europe into one liquidity zone, in real time. PIX (Brazil): Mass‑Market Instant Payments at Planetary Scale Launched in 2020, PIX is one of the fastest‑adopted real‑time payment systems in history. It has fundamentally reconfigured Brazil’s financial landscape. PIX processed tens of billions of instant transactions by 2024 and continues accelerating. [imali.app] Why PIX Matters PIX isn’t just a payment rail—it’s a behavioral shift: Near‑universal adoption QR‑based payments everywhere Instant merchant settlement Mandatory participation for major institutions PIX shows what happens when instant payments become a default, not an option:cash usage collapses, card fees come under pressure, and small businesses gain real‑time cashflow superpowers. How Real‑Time Payment Systems Actually Work Despite geographic differences, the workflow is nearly identical across RTP, SEPA Instant, PIX, FedNow, UPI, and others: Initiation – User triggers payment via bank, app, API Authorization – Funds, identity, fraud checks Network transmission – Payment routed instantly Clearing & settlement – Final within seconds Confirmation – Sender and receiver notified immediately This unified pattern explains why instant payments scale so effectively across borders. [mastercard.com] Instant Treasury: The Operator’s Advantage Real‑time payments don’t merely speed up transactions—they rewrite treasury fundamentals. 1. Liquidity Becomes Continuous With real‑time settlement: Cash concentration becomes dynamic Treasury no longer waits for bank hours Businesses can disburse funds at the last responsible moment This moves treasury from “managing float” to “orchestrating liquidity.” [thepaypers.com] 2. Real‑Time Receivables Transform Working Capital Immediate settlement means: Faster order fulfillment Reduced Days Sales Outstanding (DSO) Precise short‑term forecasting PIX and SEPA Instant have already demonstrated materially improved cash cycles for SMEs. [mastercard.com] 3. Automation Through Data RTP and SEPA Instant use ISO 20022, enabling: Automated reconciliation Clean audit trails Lower errors Rich metadata for treasury analytics RTP highlights real‑time reconciliation as a core feature. [glenbrook.com] 4. Treasury Must Now Operate “Always On” Instant rails require: 24/7 fraud monitoring Automated exception handling Systems that react in real time Legacy treasury processes—built for banking hours—don’t survive in this environment. The shift is already underway. [imali.app] A Comparative Snapshot System Limit Coverage Key Advantage RTP (US) Up to $10M [glenbrook.com] U.S. High‑value treasury payments SEPA Instant €100,000 [mastercard.com] Eurozone Pan‑EU real‑time liquidity PIX Varies Brazil Universal adoption + QR commerce The Operator’s Takeaway Real‑time payments aren’t speeding anything up—they’re compressing the financial world into a continuous system. RTP, SEPA Instant, and PIX each illustrate a different dimension of this shift: RTP shows instant liquidity at enterprise scale. SEPA Instant shows cross‑border interoperability in a unified region. PIX shows mass‑market instant adoption transforming a whole economy. If card payments digitized commerce, real‑time payments are now digitizing cashflow itself. This is the real unlock:Instant payments collapse the distance between decision and outcome.That’s the new operating advantage for the next generation of SMBs, platforms, and fintech infrastructure builders.

Agentic Commerce 101 for Beginners

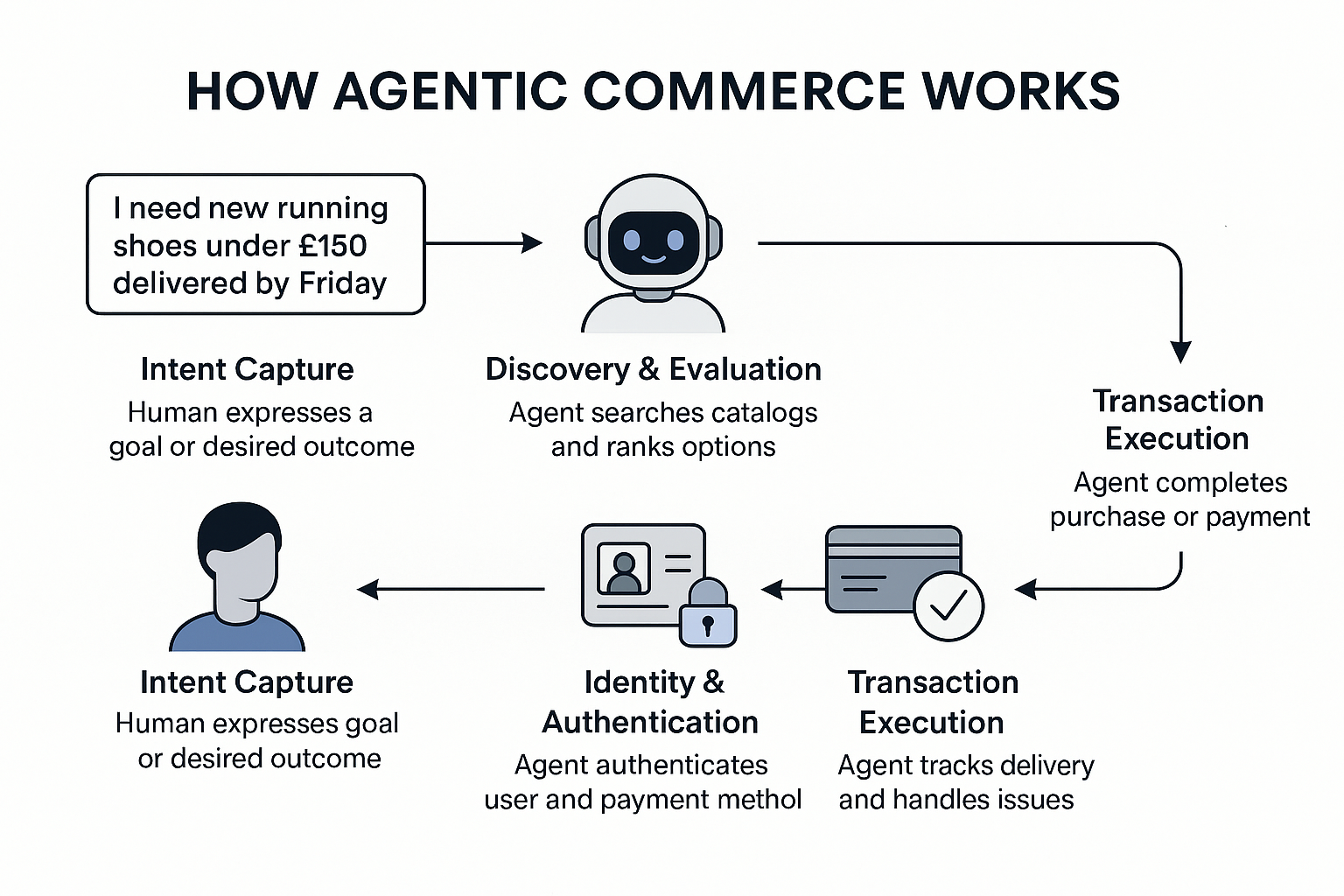

Agentic Commerce 101 for Beginners VogueBoost.com — FinTech Upskilling Series Agentic commerce is one of those shifts that sounds abstract until suddenly it feels inevitable. Much like the transition from desktop to mobile, or from cheques to instant payments, it starts with a small change in consumer expectations and then cascades into a fundamental redesign of the entire commercial stack. And as we step into 2026, it’s clear we are no longer at the “prediction” stage. The infrastructure is real, the adoption curves are rising, and both global platforms and small businesses are re‑architecting around it. To understand this shift, it helps to begin with the simplest possible framing: agentic commerce is what happens when people no longer shop — their agents do. McKinsey describes this new model as a “seismic shift,” one where AI agents don’t merely recommend products but actually anticipate needs, evaluate options, negotiate tradeoffs, and execute purchases with very little human intervention. It’s a step beyond e‑commerce, beyond chatbots, beyond “AI-powered search.” It’s a world where shopping becomes intent‑driven rather than task‑driven. A helpful way to picture it is to imagine giving a single instruction — “I need running shoes under £150 delivered by Friday” — and then stepping away. The agent interprets your intent, reviews merchant catalogs, compares prices and delivery windows, authenticates your identity, completes the transaction, and even manages the delivery or returns. As FinTech Futures notes, the key difference between agentic commerce and earlier “AI shopping assistants” is agency itself: these agents don’t just advise; they actually complete the workflow end‑to‑end. The signs are here for quite some time This shift isn’t happening in a vacuum. Over the last 24 months, we’ve seen the technical and commercial foundations assemble rapidly. Google launched its Universal Commerce Protocol in January 2026, opening a standard way for agents to interact with merchant data and perform purchases. Microsoft rolled out Copilot Checkout across the U.S. soon after. Shopify reported staggering growth — a fifteen‑fold increase — in orders initiated by AI-driven searches. Meanwhile, ChatGPT’s Agentic Commerce Protocol is now powering shopping interactions for its 900 million weekly active users. All of these developments, as nShift details, point toward a digital ecosystem that has quietly reorganized itself around machine-driven intermediaries. So what exactly is happening behind the scenes when an agent executes a purchase? The process begins with intention. Unlike legacy chatbots that respond to questions, agentic systems start with a goal: find me, decide for me, buy for me. FinTech Futures gives the simple example of a consumer specifying: “Find me shoes with blue stripes under $150,” and the agent taking responsibility for the entire subsequent workflow — discovery, evaluation, checkout, payment, even tracking. The user is no longer hunting through dozens of pages or worrying about form fields; they simply express constraints and desired outcomes. The discovery Once intent is defined, the agent begins discovery. This is where the dynamics of commerce fundamentally change. In the traditional model, discovery is mediated by scrolling, filtering, SEO, and advertising. But for an AI agent, browsing is not browsing — it’s a direct, structured sweep through inventory data, APIs, and realtime availability feeds. nShift calls the search bar “a tax on your customer’s time,” something agents remove entirely by filtering the entire commerce universe programmatically. That shift in behavior also means businesses must represent their offerings in structured, machine-readable ways or risk becoming invisible to the agents that are increasingly making purchase decisions. After the agent evaluates options, it must authenticate and transact. The mechanics here are increasingly standardized thanks to emerging interoperability frameworks. McKinsey highlights several of the major enabling protocols — the Model Context Protocol (MCP), Agent-to-Agent Protocol (A2A), Agent Payments Protocol (AP2), and Agentic Commerce Protocol (ACP). These standards together enable agents to exchange information, coordinate across systems, and, crucially, ride on the rails of existing digital commerce and payment networks. This means an agent doesn’t need a special “agent-only” checkout. It simply acts as a highly capable user moving through the same rails humans do — card payments, instant payments (RTP, SEPA Instant, Pix), bank transfers, and stablecoin rails. Once the transaction is done, the agent continues onward: tracking delivery, notifying the user, initiating returns, issuing refunds, or escalating support cases. This post‑purchase capability is especially emphasized in the newest analyses of agentic AI for SMBs, where autonomous systems can already resolve customer issues, modify shipments, send invoices, or update internal systems without human supervision. A new operating model If this sounds like an entirely new operating model, that’s because it is. And it introduces a major challenge for the market: the agentic readiness gap. As nShift explains, most retailers have spent years optimizing for discovery — SEO, ads, site design — but very few have optimized for agents that expect reliable data, trustworthy delivery, and structurally sound operational systems. Agents don’t have brand loyalty or sentiment; they evaluate merchants based on reliability signals that can be assessed instantly: delivery guarantees, stock accuracy, pricing consistency, refund policies, and frictionless integration. If a merchant’s data is poor or their fulfillment is inconsistent, the agent downranks them. Simply put: if your business isn’t machine-readable and machine-reliable, you are likely to vanish from the new purchase pathways. Beyond e‑commerce Beyond e‑commerce, the rise of agentic systems is having a transformative impact on SMB operations. The Rapid Architect report offers a vivid example: imagine walking into the office on Monday and finding your AI agent has already resolved dozens of customer inquiries, scheduled meetings, sent invoices, and flagged potential issues. This is not a hypothetical — it’s happening today. Autonomous agents represent a profound shift from passive AI tools to “executors” that complete multi-step tasks. Rather than responding to prompts, they pursue objectives. This makes them especially powerful for small teams that historically needed more staff to scale their operations. This evolution also creates new differentiation points in the market. According to BigCommerce, the platforms best positioned for this new world are those built on open, composable

A New Time of SMB Cyber Resilience: Why 2026 Marks a Turning Point in FinTech Security

A New Time of SMB Cyber Resilience: Why 2026 Marks a Turning Point in FinTech Security In 2026, something profound is happening in the world of small business. The quiet assumption that “cybersecurity is an enterprise problem” has collapsed. For the first time, cybersecurity is moving from a technical afterthought to a front‑line financial decision for small and midsized businesses. And if you’re running an SMB—whether you’re a two‑person consultancy, a growing e‑commerce brand, or a 50‑person services firm—this shift will shape how you operate, compete, and defend your future. A landmark signal of this shift arrived earlier this year when Cloudflare and Mastercard announced a strategic partnership designed specifically to strengthen cyber resilience for small businesses. The initiative isn’t about adding yet another security tool; it’s about simplifying and unifying what has become a fractured, risky, and increasingly unmanageable digital footprint for SMBs. fintech.global(https://fintech.global/2026/02/18/cloudflare-and-mastercard-target-smb-cyber-risks/) This moment matters—not just because two industry giants are integrating capabilities, but because it highlights a deeper truth: FinTech is now inseparable from cybersecurity. And for SMBs, this alignment is reshaping how trust is built, how transactions happen, and how companies navigate risk in an AI‑first world. Let’s break down what is changing—and what SMBs must do next. 1. The Hidden Cyber Blind Spots SMBs Can No Longer Ignore Over the last decade, SMBs have embraced cloud tools, digital payments, automation apps, and distributed work. This rapid adoption has delivered massive productivity but has also quietly carved out a dangerous terrain: fragmented attack surfaces. Cloudflare and Mastercard’s partnership speaks directly to this problem. As businesses add vendors, outsource services, accumulate shadow IT, and rely on legacy systems, they unknowingly create digital assets that no one is monitoring. Mastercard’s Recorded Future and RiskRecon bring threat intelligence and third‑party risk data, while Cloudflare’s Application Security platform brings defensive capabilities—all in a unified system designed to illuminate these blind spots. fintech.global(https://fintech.global/2026/02/18/cloudflare-and-mastercard-target-smb-cyber-risks/) This isn’t merely technical. It’s financial.A single exposed domain, forgotten API gateway, or outdated plugin can lead to: Payment fraud Business email compromise Regulatory fines Customer churn due to trust erosion Liability claims—especially in industries handling sensitive data For SMBs, the stakes aren’t theoretical. A breach isn’t an IT problem; it’s a business continuity problem. 2. The Financial Meaning of Cybersecurity Has Changed 2026 marks the first year where cyber risk becomes a top‑three financial risk for SMBs, not because of fear—but because of economics. Three forces are converging: a. Attackers are using AI to automate exploitation As Cloudflare notes, attackers now probe systems continuously, using automated tools that test for vulnerabilities across thousands of potential entry points. The age of a “human hacker testing a door” is over. b. Regulatory pressure is rising globally From EU DORA enforcement to China’s AML monitoring rules to the UK’s updated safeguarding framework for payment institutions coming into force in May 2026, compliance expectations are tightening for firms of all sizes.SMBs, whether they intend to or not, are now part of regulated digital ecosystems. mambu.com(https://mambu.com/en/insights/articles/payments-regulation-in-2026-key-deadlines-and-events-to-watch) c. The adoption of digital payments & financial infrastructure is exploding SMBs now use more payment intermediaries, embedded finance tools, and AI‑driven systems. Each connection is both an enabler and a risk node. Cybersecurity is no longer “technical hygiene.” It is the new cost of doing digital business. 3. Why the Cloudflare–Mastercard Partnership Is a Blueprint for the Future SMB Stack The partnership introduces three major capabilities, each of which maps directly to SMB needs:fintech.global(https://fintech.global/2026/02/18/cloudflare-and-mastercard-target-smb-cyber-risks/) 1. Eliminating Blind Spots The system monitors a company’s entire digital presence, automatically discovering internet‑facing software stacks, domains, and misconfigured assets—especially those SMBs didn’t know existed. This is transformative because most SMB breaches start with “unknown unknowns.” 2. Real‑time Security Ratings Businesses receive an A–F graded security rating based on vulnerabilities, authentication weaknesses, exposed infrastructure, and third‑party risks. This rating becomes: A KPI for board or founder oversight A credibility marker for partners A negotiation tool for cyber‑insurance premiums A benchmark for continuous improvement For SMBs without a security team, this is equivalent to getting a live diagnostic of your risk posture. 3. One‑click Risk Mitigation Once risks are identified, Cloudflare’s controls—firewalls, automated defenses, access control policies—can be activated instantly. The value here is speed.In cyber, timing determines cost.A vulnerability open for 30 days is exponentially more dangerous than one closed within hours. This partnership therefore shifts SMB cybersecurity from reactive firefighting to proactive financial risk management. 4. Why SMBs Are Especially Vulnerable in 2026 A few industry dynamics make this year uniquely challenging. a. The attack surface is expanding faster than SMBs can manage Businesses adopting AI, automation, customer portals, or even simple website plugins multiply their exposure. b. Small businesses are targeted precisely because they lack resources Attackers understand that SMBs often lack dedicated security teams—and exploit that gap. c. Payments are increasingly digital—and increasingly attractive to attackers Everything from ACH transfers to embedded checkout flows introduces new fraud vectors. d. Supply‑chain breaches disproportionately hit SMBs Dependence on SaaS tools means an upstream vendor breach often becomes your breach. The Cloudflare–Mastercard model addresses these realities by treating SMBs not as oversized consumers, but as enterprises with real, multi‑layered risk. 5. The New SMB Security Playbook for 2026 (Actionable Steps) Inspired by the insights from the partnership and broader FinTech trends, here is the Vogue Boost SMB Security Playbook for the year ahead: Step 1: Map Your Digital Footprint If you don’t know everything that connects to your business, you can’t protect it. Action: Conduct a digital asset inventory—domains, plugins, SaaS apps, APIs, vendors. Step 2: Implement Continuous Threat Visibility Tools that scan once a year are outdated. SMBs need real‑time monitoring. The Cloudflare–Mastercard model is one example, but whichever system you choose, make sure it includes: External attack surface monitoring Third‑party risk scanning Vulnerability prioritization Step 3: Shift From Perimeter Security to Zero Trust‑Like Policies Every device, employee, vendor, and connection must be verified continuously. This doesn’t require enterprise budgets—just smart adoption of: Multi‑factor authentication Identity access management Least‑privilege access controls Step 4: Treat Cybersecurity as

Why Gen Z Small‑Business Owners Still Rely on Cash — And What FinTech Must Fix Next

Why Gen Z Small‑Business Owners Still Rely on Cash — And What FinTech Must Fix Next Over the last decade, the global FinTech ecosystem has focused intensely on creating sleek, frictionless digital experiences—instant consumer payments, app‑based banking, personal credit algorithms, automated savings, and AI‑driven financial coaching. Yet when you examine how Gen Z small‑business owners actually run their companies, a surprising pattern emerges. Despite being the most digital‑native generation in history, Gen Z founders continue to lean heavily on cash transactions. Mastercard’s recent insight confirms that 52% of payments made by Gen Z SMBs are still in cash, far higher than what anyone expected from the generation raised on mobile wallets and tap‑to‑pay convenience. stocktitan.net(https://www.stocktitan.net/news/TRV/simply-business-wins-smb-insur-tech-solution-of-the-year-in-fin-tech-ucd4be2v95kg.html) But the shock doesn’t end there. Only 20% of Gen Z entrepreneurs currently have a business credit card, a number largely driven by thin‑file credit histories that block access to traditional financing channels. stocktitan.net(https://www.stocktitan.net/news/TRV/simply-business-wins-smb-insur-tech-solution-of-the-year-in-fin-tech-ucd4be2v95kg.html) It’s easy to assume this is a preference issue or a generational quirk. In reality, it reveals something deeper about the state of SMB financial infrastructure—and the gaps FinTech still hasn’t solved. In this Vogue Boost long‑form signal, we unpack why Gen Z relies on cash, what this says about SMB financial tools, and where the biggest opportunities lie for founders, operators, and FinTech builders. The Digital Paradox: The Most Online Generation Is Still Operating Offline On the surface, Gen Z’s relationship with money is profoundly digital. They pay friends instantly, use mobile banking as their default interface, deploy budgeting apps, and treat digital wallets as an extension of their identity. Yet when they step into the world of entrepreneurship, the landscape looks very different. Mastercard’s findings highlight the paradox: the same entrepreneurs who run their personal lives digitally are running their businesses in a surprisingly manual way. Cash is used because it offers immediacy, liquidity, and complete certainty at the point of transaction. stocktitan.net(https://www.stocktitan.net/news/TRV/simply-business-wins-smb-insur-tech-solution-of-the-year-in-fin-tech-ucd4be2v95kg.html) Why does this matter? Because it reveals a core truth about financial tools that support SMBs today:consumer FinTech is vastly more advanced than SMB FinTech. Gen Z is not resisting technology. They are compensating for financial infrastructure that does not meet their operational realities. The Structural Problem: SMB Financial Infrastructure Hasn’t Caught Up This isn’t about resisting modernity. It’s about solving practical problems. For Gen Z founders, cash solves three critical needs: 1. Instant Liquidity Small businesses—particularly new ones—operate on razor‑thin margins. Cash ensures that funds are available immediately, without settlement delays, batching windows, or pending statuses that can interrupt operations. 2. Certainty and Control Digital payments often introduce ambiguity. When will funds land? Is a payout delayed? Is the platform holding reserves? Cash eliminates uncertainty, allowing Gen Z founders to stay in control. 3. A workaround for broken or inaccessible credit infrastructure With only 20% of Gen Z SMBs holding a business credit card, many founders experience a liquidity gap that digital systems cannot fill. stocktitan.net(https://www.stocktitan.net/news/TRV/simply-business-wins-smb-insur-tech-solution-of-the-year-in-fin-tech-ucd4be2v95kg.html) Meanwhile, consumer FinTech has become incredibly mature—instant peer‑to‑peer transfers, real‑time alerts, transparent timelines. SMB FinTech, however, remains fragmented, slow, and often designed around legacy systems. This disparity forces Gen Z entrepreneurs into analog behaviors, even when they would prefer digital tools. The Cash Reality: What Mastercard’s Findings Really Tell Us To understand the broader context, consider Mastercard’s perspective:Gen Z’s dependency on cash stems not from nostalgia but from practicality. Cash remains a fast solution to immediate liquidity needs. It ensures smooth day‑to‑day operations in environments where digital tools introduce friction or fail to meet baseline expectations for reliability. stocktitan.net(https://www.stocktitan.net/news/TRV/simply-business-wins-smb-insur-tech-solution-of-the-year-in-fin-tech-ucd4be2v95kg.html) Mastercard’s analysis makes something else clear:SMB financial infrastructure is the lagging piece of the FinTech puzzle. Consumer FinTech has sprinted ahead. SMB FinTech has limped behind. The digital divide between personal finance tools and business finance tools is widening, and it directly shapes how young entrepreneurs behave. Gen Z’s Expectations: What Young Founders Actually Want from FinTech If FinTech wants to shift this behaviour, it must focus on how Gen Z defines value. Young founders expect: Real‑time movement of money Predictable settlement timelines (no uncertainty windows) Clear, real‑time visibility into liquidity Tools that integrate directly with their workflows Credit products designed for thin‑file applicants When these expectations are unmet, cash wins by default because it is simple, transparent, and immediate. For Gen Z founders, financial tools are not about brand familiarity or loyalty. They’re about operational dependability. A Wider View: How Cyber and Infrastructure Friction Compounds the Problem Zooming out, broader ecosystem shifts reinforce the need for simpler, more reliable financial processes. For example, cyber‑risk complexity for SMBs has increased significantly as they expand their digital footprint. Cloudflare and Mastercard’s partnership reveals the scale of blind spots SMBs face as they adopt more digital tools, integrations, and vendors. The collaboration aims to help small businesses identify and mitigate hidden cyber exposures that accumulate as they adopt cloud services and third‑party software. pymnts.com(https://www.pymnts.com/smbs/2026/mastercard-warns-credit-gap-is-holding-back-gen-z-small-businesses/) This reinforces a core point:the more complex digital operations become, the more SMBs gravitate toward methods that feel simple and trustworthy—like cash. The challenge for FinTech is not just usability. It’s building tools that deliver reliability, control, and clarity in environments where digital complexity is growing. Practical Guidance for SMB Owners Navigating Today’s Financial Tools Free or higher Membership Required. More content is available after subscription. FREE Membership Available. You must be a Free OR Paid member to access this content. View Membership Levels If you’re a small‑business owner, especially a first‑time Gen Z founder, here’s a practical roadmap to modernizing your financial operations without losing the dependability you associate with cash. 1. Map Your Cash‑Flow Friction Points Before migrating to digital tools, identify exactly where things break down. Is the issue payout timing? Fees? Delayed settlements? Reconciliation overhead? Understanding friction points helps you choose tools that genuinely improve operations. 2. Prioritize Certainty Over Novelty Don’t be swayed by flashy features. Choose platforms that offer: Guaranteed payout times Real‑time transaction data Transparent settlement policies Certainty is more valuable than optional extras. 3. Start Building a Thin‑File Credit Profile Early Because only 20% of Gen Z SMBs

Decoding the Silent Revenue Killer: Infographic

Churn-Shield Benchmark Report | Interactive Infographic ⯈ ChurnShield Benchmarks Root Causes Risk Matrix Framework 2026 Intelligence Report Decoding the Silent Revenue Killer Customer churn isn’t just a metric; it’s a compounding leak in your business model. Explore the definitive benchmark data to understand why customers leave and how to build an impenetrable retention shield. 14.2% Average SMB Churn $2.4M Avg Annual Lost Revenue 68% Categorized as Preventable The Industry Baseline Before implementing defensive strategies, it is crucial to understand the macroeconomic landscape. The chart below illustrates the average annual churn rates across distinct business sectors. This data serves as the baseline against which you should measure your own retention performance. High-velocity transactional businesses naturally experience higher turnover than integrated enterprise solutions. Annual Churn Volume by Sector Percentage of customer base lost annually across key SMB verticals. ➤ B2B SaaS Resilience: Operating at the lowest churn tier (5.8%), B2B SaaS benefits from high integration costs and subscription-based friction, making them highly resilient to impulse cancellations. ➤ Retail Volatility: Retail and E-commerce face extreme volatility (24.5%) due to near-zero switching costs and hyper-competitive market saturation. Anatomy of Defection Identifying the volume of lost customers is only the first step. To build an effective shield, we must dissect the why. Our analysis categorizes churn into five primary drivers. Notably, the majority of churn is not driven by product failure or pricing, but by experiential friction during the customer lifecycle. The visualization below breaks down these root causes. Primary Drivers of Cancellation 🚩 The Onboarding Failure (38%) The absolute largest driver of churn. If a user does not achieve their “first value” within 14 days of acquisition, the probability of churn triples. They leave because they never understood how to win using your product. 💬 Support Friction (24%) Customers expect issues; they do not tolerate prolonged resolution times. Forcing customers to repeat their problems across multiple channels is a primary catalyst for immediate cancellation. 💸 Value Degradation (18%) Often mislabeled as “too expensive.” Customers leave when the perceived return on investment dips below the subscription cost over time due to a lack of continuous feature adoption. The Health Risk Matrix Proactive retention requires identifying at-risk accounts before they cancel. By plotting a cohort of users based on their internal Health Score against their Monthly Recurring Revenue (MRR), we reveal the hidden danger zones. The bubble chart below illustrates this relationship. Accounts in the upper-left quadrant represent critical revenue at imminent risk of loss. ↑ High Value ← High Risk Account Vulnerability Correlation Bubble Size = Relative Account Age. Left = Danger Zone. The Mitigation Framework Data without action is mere trivia. Based on the behaviors of top-quartile retention organizations, we have synthesized a three-stage architectural framework to halt defection. Implement these procedural steps to transform your customer lifecycle from a leaky funnel into an expanding revenue engine. 01 Accelerate First Value Restructure the first 30 days. Shift focus from product tutorials to specific outcome achievements. ✓ Mandatory Guided Onboarding ✓ Measure ‘Time-to-Value’ strictly ✓ Proactive Day-14 check-in calls 02 Predictive Intervention Move support from reactive troubleshooting to proactive health monitoring and immediate outreach. ✓ Implement dynamic Health Scores ✓ Alerts for 7-day usage drops ✓ Empower agents with instant credit 03 Continuous ROI Proof Never assume the customer remembers why they bought. Prove the value continuously. ✓ Automated Monthly Value Reports ✓ Quarterly Business Reviews (QBRs) ✓ Exclusive access for tenured clients Stop the leak. Secure the revenue. Download Full Executive Brief © 2026 Churn-Shield Analytics. Generated for Interactive Infographic Demo.